The End of Easy Beta: Navigating a Market That Demands Selectivity

The Macro View: A More Selective Market Emerges

By David Miller, Co-Founder and Chief Investment Officer, Catalyst Capital Advisors LLC and Rational Advisors, Inc.

Macro Outlook

The market is entering a period where macro, not momentum, is, in our opinion, likely to drive returns. A big issue is that investors are now trying to handicap whether the Middle East shock, even after the recent ceasefire, becomes a short-lived geopolitical spike or a more durable inflationary event. If oil continues to retreat and the conflict truly does de-escalate, equities have room to recover because the first quarter already reflected a meaningful repricing of geopolitical and inflation risk.

However, if energy remains elevated, Q2 becomes much more challenging because higher fuel costs start to pressure margins, consumer spending, and the Fed’s flexibility all at once. Recent reporting and Fed-related data suggest exactly that tension: markets are hoping for de-escalation, while inflation nowcasts are already showing war-related pressure on headline prices.

A Selective Market Could Mean a Rising Tide Does Not Lift All Boats

My base case is that Q2 could be a more selective market than investors got used to in prior rallies. This is probably not the kind of backdrop where everything rises together. If rates stay higher for longer and inflation stays sticky, leadership should favor businesses with pricing power, durable free cash flow, and balance-sheet strength, while more rate-sensitive and lower-quality parts of the market remain vulnerable.

In other words, investors may still want exposure, but they are likely to become much less forgiving about valuation and much more focused on earnings durability. That matters because the Fed does not appear eager to change course quickly, even as markets debate whether the next move is a cut, a long pause, or in more extreme scenarios even a hike if inflation worsens.

Can the Consumer Economy Absorb a Shock?

The consumer will be one of the key swing factors this quarter. So far, the economy has held up better than many expected, with February retail sales coming in solidly, but there is a real question about how long that resilience lasts if gasoline prices stay elevated and broader cost pressures continue feeding through the system.

That is why I think Q2 is less about broad optimism and more about whether the U.S. economy can absorb an external shock without rolling over. If the consumer remains intact, the market can stabilize. If not, investors will start worrying more seriously about margin compression and slower growth into the back half of the year.

Bottom Line: Volatility Ahead

Expect volatility, expect narrower leadership, and expect markets to stay highly headline-sensitive. A benign outcome is still possible, especially if oil keeps falling and inflation pressure proves temporary.

But this is not a clean “risk-on” environment yet. It is a market that wants to rally, but still needs confirmation from energy prices, inflation data, and the Fed before investors can feel confident.

Mr. Miller is a portfolio manager for the Catalyst Systematic Alpha Fund (ATRFX), Catalyst Insider Buying Fund (INSIX), Catalyst Insider Income Fund (IIXIX), Rational Strategic Allocation Fund (RHSIX) and the Strategy Shares Gold Enhanced Yield ETF (GOLY).

Macro and Structural Pressures Likely to Sustain Elevated Volatility

By Roy Niederhoffer, Founder & President, R. G. Niederhoffer Capital Management

Equity Outlook

While the Iran war spiked volatility in March, there are other factors ruminating that seem likely to keep markets volatile well into Q2 and beyond.

Although a recent ceasefire may begin to ease some of the pressure, the Strait of Hormuz remains effectively closed, with roughly 800 tankers stranded and Iran permitting only selective passage. Even with the ceasefire, re-opening commercial shipping will take months. Brent is above $110 and WTI near $99, gas has moved from $2.93 to $3.88 in a single month, and disrupted shipping is adding costs across the supply chain. The strain on a consumer already stretched by years of cumulative inflation is likely to intensify.

The Fed has shifted to a hawkish lean, and with consumer price pressure and a 10% global tariff, easing is unlikely, particularly with nearly $40T of debt to service. Oil has already spiked, however, and this is not a situation where we might expect prices to rise indefinitely.

What makes the current dislocation particularly interesting is the speed of narrative rotation. Within a single month, the dominant market story shifted from AI monetization concerns to geopolitical supply shock to stagflation risk to tentative peace optimism. Each rotation forces a repricing. Each repricing triggers the same cognitive reflexes: recency bias drives momentum chasers into the trade just as it reverses; loss aversion forces liquidation at precisely the wrong moment; anchoring to pre-crisis levels creates a false sense of how far markets can move.

The Stressed Private Credit Market

Private credit remains under stress, with the Cliffwater BDC Index down -19% since July and 25 to 40% of private credit concentrated in software, the sector most threatened by AI disruption. At conferences, private credit managers are touting dispersion of returns: “It’s not us, it’s those other bad managers.” When an industry competes on relative survival rather than absolute merit, it has a problem.

The stock-bond correlation has remained positive since 2021, meaning fixed income allocations add equity beta rather than reduce it. The S&P beta of a 60/40 portfolio has climbed to +0.71 since 2020, from +0.50 over the prior two decades. And underneath the major indices, single-stock realized volatility versus the index is at a record, as the market prices in the AI transformation per company.

And yet the right tail must also be considered. The U.S. runs deficits of 6% of GDP, and with $40 trillion in debt, asset prices could rise merely because their denominator loses value. The midterms and the government’s inability to tolerate austerity suggest the new Fed Chair may take a more accommodative stance, creating an upside surprise for stocks.

At Niederhoffer, our overlay strategy is designed to provide upside enhancement as well as downside risk mitigation. Since inflation returned post-Covid, the S&P has been up in 5 of 6 years at double its average return, and this may be the norm as the dollar debases.

Bottom Line

We believe that factors driving increased two-sided volatility are likely to persist well beyond the current quarter.

Dual Shocks Drive a Shift in Credit Sentiment

By Natalia Lojevsky & Stan Sokolowski, CIFC Asset Management

The first quarter closed on a decidedly more cautious note than it began. Two successive shocks reshaped investor psychology across credit markets: first, the rapid repricing of the Technology and Software complex as concerns about AI-driven disintermediation spread from sector to sector with unusual speed, and second, the outbreak of armed conflict in the Middle East, which sent oil prices sharply higher and closed the Strait of Hormuz to commercial shipping.

The geopolitical dimension, still very much unresolved as we enter the second quarter, has materially altered the inflation and rate-path calculus for investors. What had been a relatively constructive backdrop for credit entering 2026 gave way to a more complex one, as rising energy costs reignited inflation expectations and all but eliminated the near-term prospect of further Fed easing. Investor confidence was further tested by a wave of elevated redemption requests from semi-liquid private credit vehicles.

Against this backdrop, the senior secured corporate loan market posted its weakest first-quarter performance since 2020, though the stress was concentrated rather than systemic. Double-B loans held positive returns even in February’s most acute period of dislocation, while several defensive sectors demonstrated genuine resilience throughout and the asset class notably outperformed both equities and traditional fixed income in March.

Duration, Inflation, and Geopolitical Risk in Focus

Entering the second quarter, the key open questions facing credit investors are not primarily about credit quality but about duration and resolution. The Strait of Hormuz closure is the most immediate macro wildcard, with oil supply constraints keeping inflation expectations elevated and the likelihood of near-term rate cuts diminished considerably. Even after the ceasefire announcement, it will take some time for normalcy to return.

Technology Credit: Differentiation Likely to Replace Indiscriminate Selling

The coming weeks will also bring the first full earnings season for Software and Technology borrowers since the AI disruption narrative took hold, providing hard revenue data against which to measure fears that have, in our view, run materially ahead of underlying fundamentals.

The broad-based selloff in software loans penalized mission-critical, deeply embedded platforms alongside genuinely vulnerable point solutions — a distinction the market’s indiscriminate selling largely ignored. We are closely monitoring credits with near-term refinancing exposure and elevated AI-substitution risk and have selectively reduced positions where business model vulnerability and maturity pressure create a compounding risk profile.

At the same time, we continue to find compelling opportunities in software sub-sectors where deep domain knowledge, workflow integration, and customer relationships built over decades create durable barriers to displacement, particularly in cybersecurity, core systems of record, and vertical platforms serving risk-averse enterprise end markets.

Bottom Line: Discipline, Dispersion, and the Primacy of Carry

The macro backdrop is noisy, the list of risks is always long, and anxiety remains high, but fundamentals are broadly sound, default risk is manageable, and starting yields have potential to do a lot of work for investors willing to underwrite credit risk thoughtfully.

In a world where equity indices are concentrated in a handful of megacap names and valuations are rich, investors have a chance to rotate into credit strategies that offer the prospect of long-run equity-like returns for senior secured risk, effectively mitigating risk in the portfolio while keeping return targets intact.

Credit may not dominate the headlines the way AI or tariffs do — but in an environment like this, it remains a compelling opportunity to compound capital.

Q2 Spotlight: Energy Infrastructure

By Simon Lack, Founder, SL Advisors

Looking Back

The first quarter of 2026 has been characterized by a powerful rotation back into energy infrastructure, driven by three key forces:

- Liquified Natural Gas (LNG) Expansion Momentum

- Fee-Based Cash Flows

- Recovery from 2025 Weakness

Internally, we are heavily tilted toward LNG-linked names such as Cheniere Energy, Venture Global and NextDecade, all of which benefited from rising global gas demand and continued export capacity expansion. Midstream operators like Energy Transfer and Targa Resources also rallied as investors sought yield and inflation-resistant income streams.

After a negative 2025 return of (−7.8%), the sector entered 2026 with lower valuations, enabling a sharp re-rating as sentiment improved.

Looking Ahead

As we look ahead, we believe several catalysts are likely to shape performance in the midstream energy sector. Continued geopolitical uncertainty and energy security concerns are supporting LNG demand, particularly in Europe and Asia. Qatar, formerly the world’s #3 LNG exporter, is now a less reliable supplier after having declared force majeure and closing their facility. This can benefit US LNG exporters.

Midstream companies remain focused on returning capital rather than overbuilding, supporting equity valuations. As interest-rate-sensitive assets, midstream equities could outperform if yields stabilize or decline.

Despite strong fundamentals, several risks could impact the sector. While midstream revenues are largely fee-based, prolonged declines in oil or gas consumption could reduce volumes flowing through pipelines. Companies in this sector are growing payouts and also buying back stock. Higher rates could compress valuations, although many pipeline companies have contracts that link price increases to PPI.

Bottom Line

Given the conditions, we favor the North American LNG and midstream growth story, combining high current income with capital appreciation potential. The sector’s strong Q1 performance reflects improving sentiment, LNG tailwinds, and capital discipline across the sector.

However, its concentrated structure and sensitivity to macro variables — particularly interest rates and global energy demand — mean that while upside remains compelling into Q2, there may be times of increased volatility.

IMPORTANT DISCLOSURES

Past performance is not a guarantee of future results.

INVESTORS SHOULD CAREFULLY CONSIDER THE INVESTMENT OBJECTIVES, RISKS, CHARGES AND EXPENSES OF LIQUID ALTERNATIVE FUNDS, INCLUDING THE CATALYST FUNDS AND THE RATIONAL FUNDS. THIS AND OTHER IMPORTANT INFORMATION ABOUT A FUND IS CONTAINED IN THE PROSPECTUS, WHICH CAN BE OBTAINED BY CALLING 866-447-4228 OR AT WWW.CATALYSTMF.COM OR WWW.RATIONALMF.COM, AS APPLICABLE. THE RELEVANT PROSPECTUS SHOULD BE READ CAREFULLY BEFORE INVESTING. BOTH THE CATALYST FUNDS AND THE RATIONAL FUNDS ARE DISTRIBUTED BY NORTHERN LIGHTS DISTRIBUTORS, LLC (“NLD”). NLD HAS HAD NO ROLE IN THE STRUCTURING OR DISTRIBUTION OF ANY OTHER INVESTMENT PRODUCTS REFERENCED HEREIN, AND IS NOT RESPONSIBLE FOR THE MARKETING OR PROMOTIONAL MATERIAL RELATED TO THE OTHER INVESTMENT PRODUCTS PRODUCED OR SPONSORED BY ANY OTHER FIRM. DAVID MILLER, JOE TIGAY, DWAYNE MOYERS, MARTIN LUECK, IAIN CAMERON, STRATEGY SHARES, EQUITY ARMOR, SMH ADVISORS, AND ASPECT CAPITAL ARE NOT AFFILIATED WITH NLD AND ULTIMUS FUND SOLUTIONS.

Though the objectives, strategies and assets traded may differ significantly across liquid alternative approaches, investing in liquid alternatives generally carries certain risks. These risks may include, but are not necessarily limited to, the following: Certain funds may invest a percentage of their assets in derivatives, such as futures and options contracts. The use of such derivatives and the resulting high portfolio turn-over may expose such funds to additional risks that they would not be subject to if they invested directly in the securities and commodities underlying those derivatives. These funds may experience losses that exceed those experienced by funds that do not use futures contracts, options and hedging strategies. Investing in commodities markets may subject a fund to greater volatility than investments in traditional securities. Currency trading risks include market risk, credit risk and country risk. Foreign investing involves risks not typically associated with U.S. investments. Changes in interest rates and the liquidity of certain investments could affect a fund’s overall performance. Other risks include U.S. Government securities risks and investments in fixed income securities. Typically, a rise in interest rates causes a decline in the value of fixed income securities or derivatives owned by a fund. Furthermore, the use of leverage can magnify the potential for gain or loss and amplify the effects of market volatility on a fund’s share price. All funds are subject to regulatory change and tax risks; changes to current rules could increase costs associated with an investment in a fund.

The value of a fund may decrease in response to the activities and financial prospects of an individual security or group of securities held in a fund’s portfolio. Investments in foreign securities could subject a Fund to greater risks, including currency fluctuation, economic conditions, and different governmental and accounting standards. A fund’s portfolio may be focused on a limited number of industries, asset classes, countries or issuers. Certain funds may invest in high yield or junk bonds, which present a greater risk than bonds of higher quality. Other risks may include credit risks and interest rate risk, particularly with respect to floating rate loan funds. Changes in short-term market interest rates will directly affect the yield on the shares of a fund whose investments are normally invested in floating rate debt. Floating rate loan funds tend to be illiquid, and a fund might be unable to sell the loan in a timely manner as the secondary market is generally a private, unregulated inter-dealer or inter-bank re-sale market.

The views expressed herein are as of April 8, 2026, and represent a general guide to the perspectives of the authors. The information and opinions contained in this document have been compiled or arrived at based on sources believed to be reliable and in good faith; however, no representations or warranties of any kind are intended or should be inferred with respect to the accuracy of the information contained herein or the economic return of an investment in a fund, and no assurance can be given that existing laws will not be changed or interpreted adversely. All such information and opinions are subject to change without notice. There is no assurance that these opinions or forecasts will come to pass, and past performance is no assurance of future results.

Quality ratings reflect the credit quality of the underlying securities in the Fund’s portfolio and not that of the Fund itself. Quality ratings are subject to change. Moody’s assigns a rating of AAA as the highest to C as the lowest credit quality rating.

20260413-5376989

Download PDF

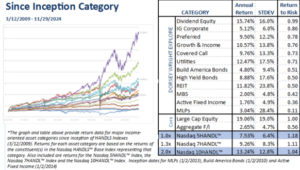

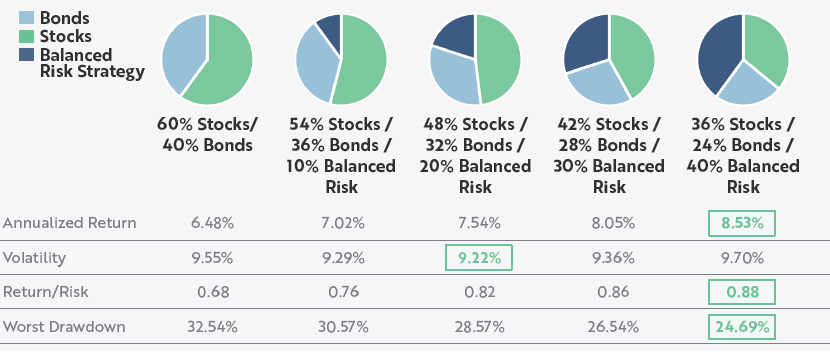

Data Source: Bloomberg LP and Catalyst Capital Advisors LLC. Based on monthly return data from 12/31/1999 to 12/31/2024. Stocks are represented by the S&P 500 TR Index; bonds are represented by the Bloomberg US Aggregate Bond Index; Balanced Risk Strategy is represented by 100% notional exposure to SG CTA Trend Index, 50% allocation to the S&P 500 and a 50% allocation to the Bloomberg US Short Treasury TR Index (to represent collateral for futures program). Rebalanced monthly. Past performance does not guarantee future results. See important disclosures at the end of this presentation, including with respect to the limitations inherent to hypothetical performance comparisons.

Data Source: Bloomberg LP and Catalyst Capital Advisors LLC. Based on monthly return data from 12/31/1999 to 12/31/2024. Stocks are represented by the S&P 500 TR Index; bonds are represented by the Bloomberg US Aggregate Bond Index; Balanced Risk Strategy is represented by 100% notional exposure to SG CTA Trend Index, 50% allocation to the S&P 500 and a 50% allocation to the Bloomberg US Short Treasury TR Index (to represent collateral for futures program). Rebalanced monthly. Past performance does not guarantee future results. See important disclosures at the end of this presentation, including with respect to the limitations inherent to hypothetical performance comparisons.